Foreign exchange trading sees fluctuations according to volatility and other market conditions. The team at Duetsche Bank has encouraging words for traders:

Here is their view, courtesy of eFXnews:

The international press is replete with stories of poor investor returns and discretionary fund closures this year. Reuters reports1 that Q1 2016 marked the first quarter of outflows from hedge funds since the financial crisis. Reports like this beg the question: is this the end of macro investing? Have FX returns structurally declined?

We attempt to answer this question by looking at the performance of the Deutsche Bank currency returns (dbCR) index, which aims to capture passive FX investing in a similar way the S&P 500 does so for equities.

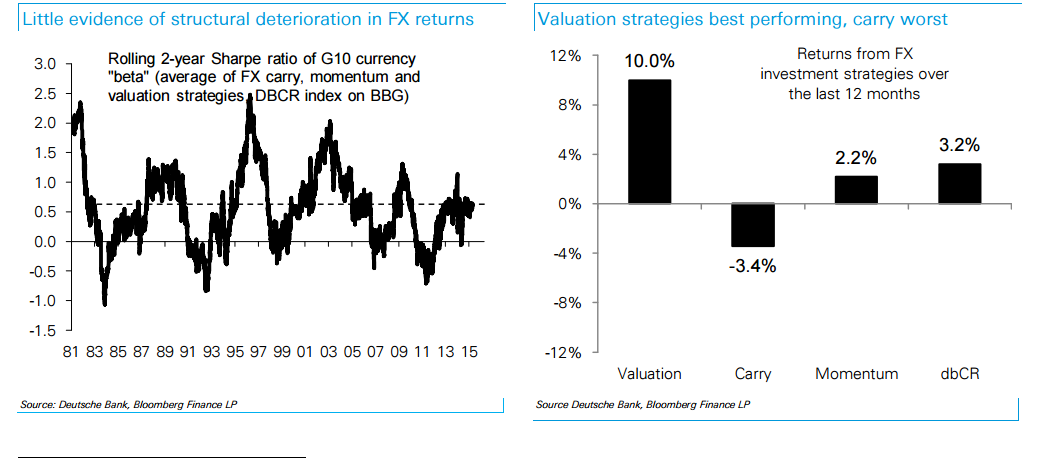

The results are striking. The index has returned a Sharpe ratio of 0.6 over the last two years almost exactly in line with its medium term average. A quick glance at the index indicates no structural decline in FX excess returns, which continue to go through cycles of over- and under-performance (chart 1).

So why are discretionary returns poor? If returns still exist, it must be that they are becoming more difficult to anticipate. After three years of major central bank-induced trends (Fed lift-off preparations, Abenomics, ECB QE), we would argue that markets are undergoing a major transition away from central banks as a driver of markets.

Declining visibility around macro trends and central banks is becoming a rising constraint. Yet there is a silver lining. History provides plenty of evidence where themes other than central bank policy have driven market trends in the past. Our best guess is that major changes to fiscal policy could be such a driver going forward. It is not the time to give up currency investing just yet.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.