Following the mixed jobs report, some see it as good enough for a rate hike in December, but not everybody agrees. Here is an opinion by Danske:

Here is their view, courtesy of eFXnews:

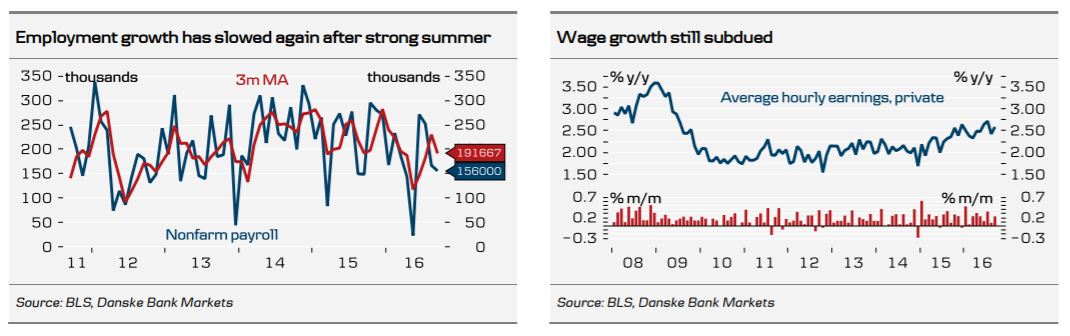

Nonfarm payrolls rose 156,000 in September, in line with our expectations of 160,000 but below consensus of 172,000. There were no big revisions to the last two months (combined -7,000). Thus it seems that the strong jobs reports in the summer were mainly due to the weakness in the spring. Employment growth was driven by the service sector, while manufacturing employment fell again. Overall, employment growth has slowed this year. On average, nonfarm payrolls have risen 180,000 per month, below the average increase in both 2015 (230,000), 2014 (250,000) and 2013 (190,000). While this may be due to the fact that we are not far from full employment, it may also be a lagged effect from the economic slowdown as GDP growth has slowed to around 1% q/q AR the past three quarters. Still, September marked the six year anniversary of the job recovery.

The details reveal there is still slack left in the labour market as the unemployment rate rose from 4.9% to 5.0% and the underemployment rate (a broader unemployment measure) was unchanged at 9.7%. The higher unemployment rate despite increasing employment is due to an increasing labour force. While it is positive that more workers are returning to the labour force (perhaps due to better employment prospects), it is also a sign that there was more slack in the labour market than previously thought. The underemployment rate has stopped declining and has been more or less constant over the last 12 months (see the chart to the right). This broader unemployment measure has previously been one of Yellen’s favourite slack measures.

Overall, the September jobs report was not the ‘smoking gun’ for the Fed. For now we stick to our non-consensus view that the Fed will stay on hold until H1 17, although it is a close call whether the Fed will hike or not in December.

The reason for our call is that the Fed seems too optimistic on Q3 GDP growth and we fear that economic data may disappoint in the short-term. The combination of weak GDP growth over the past three quarters, still slack left in the labour market, subdued wage growth, low inflation expectations and core inflation still below 2%, means that the Fed can afford to stay patient. A November hike seems unlikely due to the Presidential election just a week after the next FOMC meeting. Markets have priced in a two-thirds probability of a hike by the turn of the year.

Next week we get retail sales in September, FOMC minutes from September and Yellen is speaking. All three could be important for our Fed call.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.