This was the week: Worries, worries, worries

The safe-haven yen saw quite a bit of demand in a week that was dominated by concerns.

China kicked off the week by setting a growth target of 6-6.5% for 2019, lower than 6.6% seen in 2018, which was, in turn, the lowest in 28 years. Later in the week, China’s weak trade data also weighed on the mood.

Trade talks between China and the US did not see a breakthrough, and a summit between Presidents Donald Trump and Xi Jinping is not that close. The same goes for Brexit talks, which saw the same difficulties around the Irish Backstop. While a delay in Brexit is on the cards, the failure to reach a new accord is worrying.

The European Central Bank surprised with an early dovish twist that had an impact well beyond Europe, and so did the Bank of Canada. They joined the Fed that reiterated its patience on raising interest rates, with the Bank of Japan already deep in the dovish territory.

US data was mixed. The forward-looking ISM Non-Manufacturing PMI came out at a robust 59.7 points, showing the resilience of the economy. New Home Sales defied the downtrend in housing with 621K annualized in December. However, the broad trade balance may anger Trump that vowed to shrink it.

The US jobs report came out with a poor increase of only 20K in February against 180K projected and 311K in January. However, wage growth accelerated to 3.4% YoY, the unemployment rate dropped to 3.8% and the U-6 underemployment rate slipped to 7.3%. The USD eventually recovered from the initial slide and its prospects remain positive.

See: NFP Quick Analysis: 5 reasons why the data may provide buying opportunity on the USD

All in all, it was not a good week for stocks, and USD/JPY dropped with them.

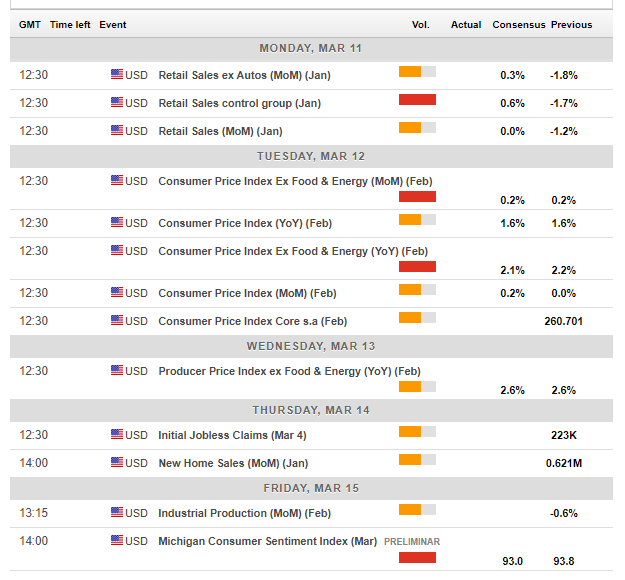

US events: Consumer data

Markets will not have a lot of time to digest the Non-Farm Payrolls report before another top-tier figure awaits it: Retail Sales for January. Once again, the data comes late due to the government shutdown.

The data for December was devastating: a fall of 1.2% in the headline and a plunge of 1.7% in the all-important Control Group. The figures did not match other reports, and entirely a few analysts cast doubt about them. January is already expected to show rises in all the measures, and markets will also watch revisions for December’s numbers quite closely. Consumption is critical to the US economy.

The next substantial release is on Tuesday with inflation numbers. The all-important Core CPI YoY remained steady at 2.2% in January, and a minor slide to 2.1% is on the cards. Headline inflation stood at 1.6% in the first month of the year, and no change is forecast for February. The steady levels of inflation allow the Fed to remain patient.

The Producer Price Index on Wednesday will provide additional insights into inflation and jobless claims on Thursday may be of interest. The final word of the week belongs to the consumer, which gets to close the week after starting it.

The University of Michigan’s preliminary Consumer Sentiment survey for March is predicted to remain steady at the 93 handles. The numbers are upbeat but off the highs around 100. Consumer confidence is considered a leading indicator of consumption.

Here are the top US events as they appear on the forex calendar:

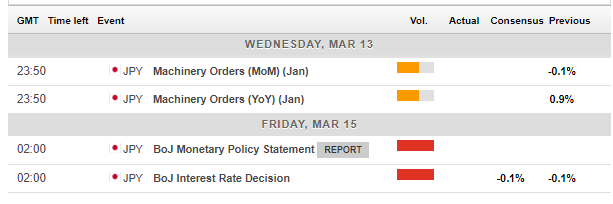

Japan: Fewer BOJ decision stands out

Trade talks between the US and China will continue moving markets and risk sentiment. Also, the critical votes in the UK Parliament on Tuesday, Wednesday, and Thursday will likely impact sentiment. If Parliament instructs the government to seek an extension to Article 50, a relief rally could boost USD/JPY.

And towards the end of the week, there is finally a notable event in Japan: the BOJ decision. Governor Haruhiko Kuroda and his colleagues stressed the importance of loose monetary policy, especially as inflation remains far from the elusive 2% target. In their decision on Friday, central bankers are not expected to introduce any new measures. The interest rate will likely remain at -0.10% and the Tokyo-based institution is projected to pledge to keep 10-year yields close to 0%.

However, the BOJ may be tempted to join its peers in some kind of a dovish twist given the economic slowdown.

Pressure on the yen may also come from the Ministry of Finance. The Japanese authorities are not happy with the rising value of the yen which makes Japanese exports less attractive. A verbal intervention could halt the fall of USD/JPY. An outright intervention is unlikely at this point.

Here are the events lined up in Japan:

USD/JPY Technical Analysis

Dollar/yen struggled to extend its gains after hitting a high of 112.12. The pair broke above the 200-day Simple Moving Average but could not keep up. The drop back below the indicator is a bearish sign. Momentum remains upbeat, and USD/JPY is trading above the 50-day SMA, so the picture remains mostly bullish.

111.00 is a round number that is fought over. Significant support awaits at 110.25 which supported the pair twice in February and separates ranges. 109.50 provided support in early February when it traded at lower ground. 109.10 had the same role in January and 108.50 was a swing low in late January.

111.45 worked as support in early March and capped the pair around Christmas. 112.12 was the recent peak mentioned earlier. It is followed by 112.60 that provided support in late 2018 and 113.10 was a cushion in December, when USD/JPY was trading on high ground.

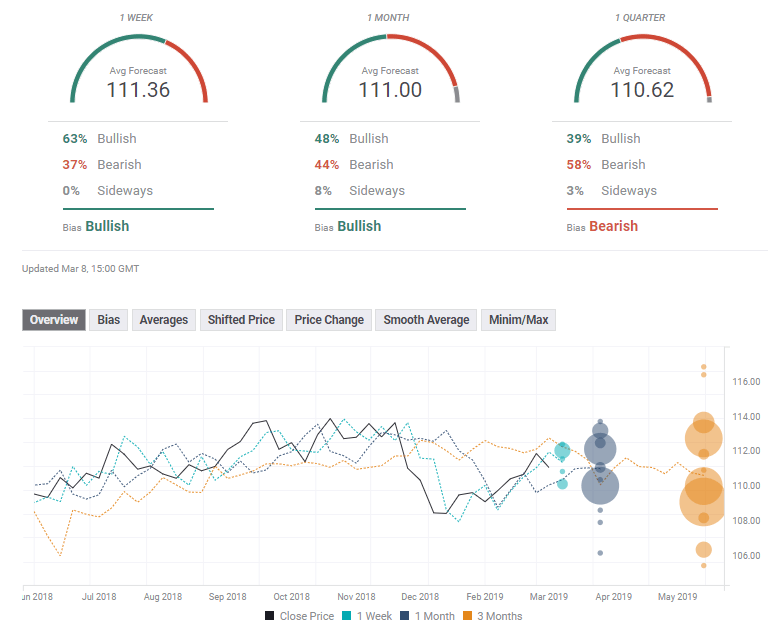

USD/JPY Sentiment

The doom and gloom are unlikely to diminish easily, despite all the help from central banks, even from the BOJ. A big breakthrough in US-Chinese talks is needed or impressive US data. And these may come in short supply.

The FXStreet forex poll of experts shows a bullish trend in the short and medium terms but a downfall afterward. The targets show a downward trajectory. The average targets are marginally lower than last week on all timeframes.

Get the 5 most predictable currency pairs