This was the week: Signs of economic recovery

Chinese GDP growth beat expectations with 6.4% annualized growth in Q1. While many doubt the veracity of the data coming from the world’s second-largest economy, there are signs that credit stimulus and investment in 5G technology help it. The news helped soothe nerves in markets.

Fed officials provided somewhat contradicting messages: James Bullard suggested the Fed should cut rates if inflation falls, while Eric Rosengren expressed satisfaction from the current economic situation.

US Industrial Production disappointed with a drop of 0.1% while the trade balance deficit narrowed.

Trade talks between the US and China continued by phone and will continue with top-level meetings between the top-negotiators. China’s Vice Premier Liu He will travel to Washington and US Trade Representative Robert Lighthizer will fly to Beijing.

Reports that the US is ceding some ground help calm the mood, but there is still no breakthrough nor a meeting set between Presidents Donald Trump and Xi Jinping.

In Japan, the trade balance surplus surprised to the upside, but the underlying data was disappointing as exports dropped more than had been expected. Industrial output also slipped.

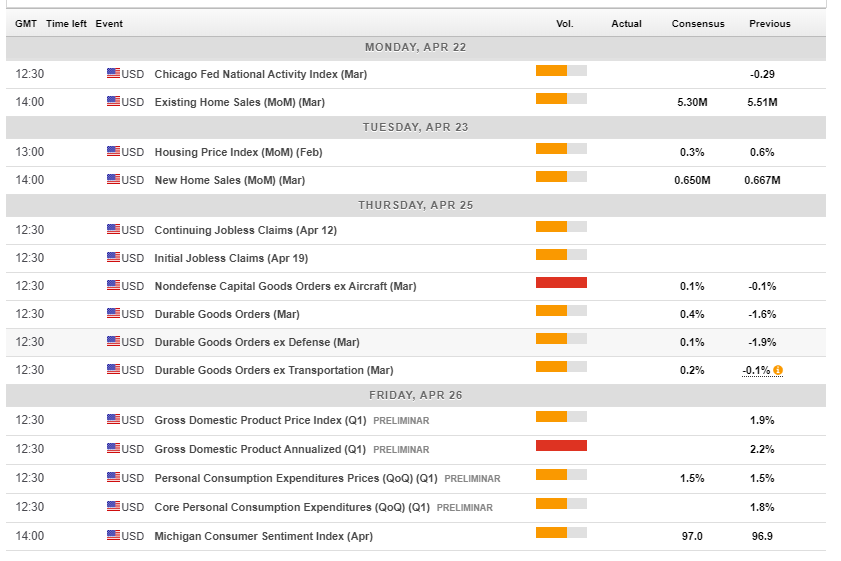

US events: Q1 GDP stands out

While most markets are on holiday on Monday, the US releases Existing Home Sales. They bounced back from the lows in February and hit an annualized level of 5.51 million units. A moderation is projected now.

New Home Sales are published on Tuesday. While sales of new units consist only a small share of the market, these transactions trigger broad economic activity. Also here, February saw a rebound, to 667K annualized units, and also here a moderation is on the cards.

Durable Goods Orders for March are published on Thursday. Headlines orders dropped by 1.6% in February but looking more closely, non-defense ex-aircraft orders slid by only 0.1%. The report provides substantial information about investment and also feeds into the GDP report on the following day.

The week culminates in Friday’s GDP report. The US economy grew by 2.2% in Q4 2018, slower than in previous quarters but better than other developed economies. Another slowdown is forecast for Q1. The first quarter usually sees more gradual growth, bad weather hit the nation, and the government shutdown also took its toll.

The big question is: by how much? The first release tends to feature the most substantial surprise and also the most significant impact on currencies.

Here are the top US events as they appear on the forex calendar:

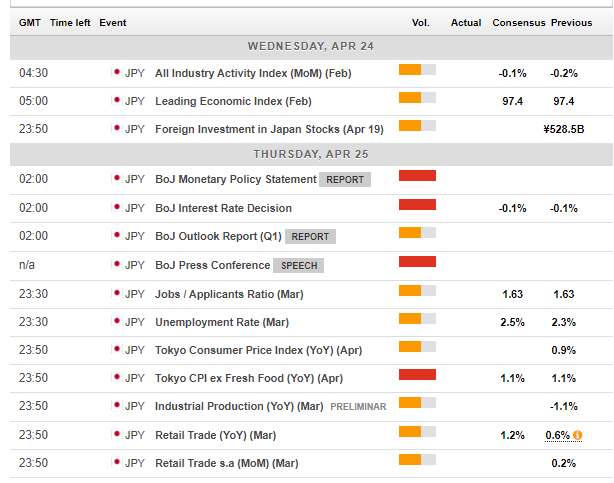

Japan: BOJ decision and fresh inflation data

The Bank of Japan’s rate decision stands out. The Tokyo-based institution will likely maintain its ultra-loose monetary policy: an interest rate of 0.1% and a pledge to hold the 10-year yield close to zero. The BOJ will also release its quarterly outlook and will probably downgrade its forecasts, following its peers.

Any hints that the BOJ is considering additional steps to boost inflation could weigh on the yen. However, Governor Haruhiko Kuroda and his colleagues do not have many tools in the shed to lift prices.

And fresh inflation figures stand out late on Thursday. The Tokyo region releases inflation data for April. Headline inflation stands at a meager 0.9% while CPI excluding Fresh Food, the “core of the core” is not doing much better with 1.1%, far from the 2% target the BOJ set.

The safe-haven yen may benefit from growing worries that North Korea is marching forward with its development of nuclear weapons and ballistic missiles. The topic has bee on the backburner so far.

USD/JPY traders need to follow bond yields and also stocks, as usual.

Here are the events lined up in Japan:

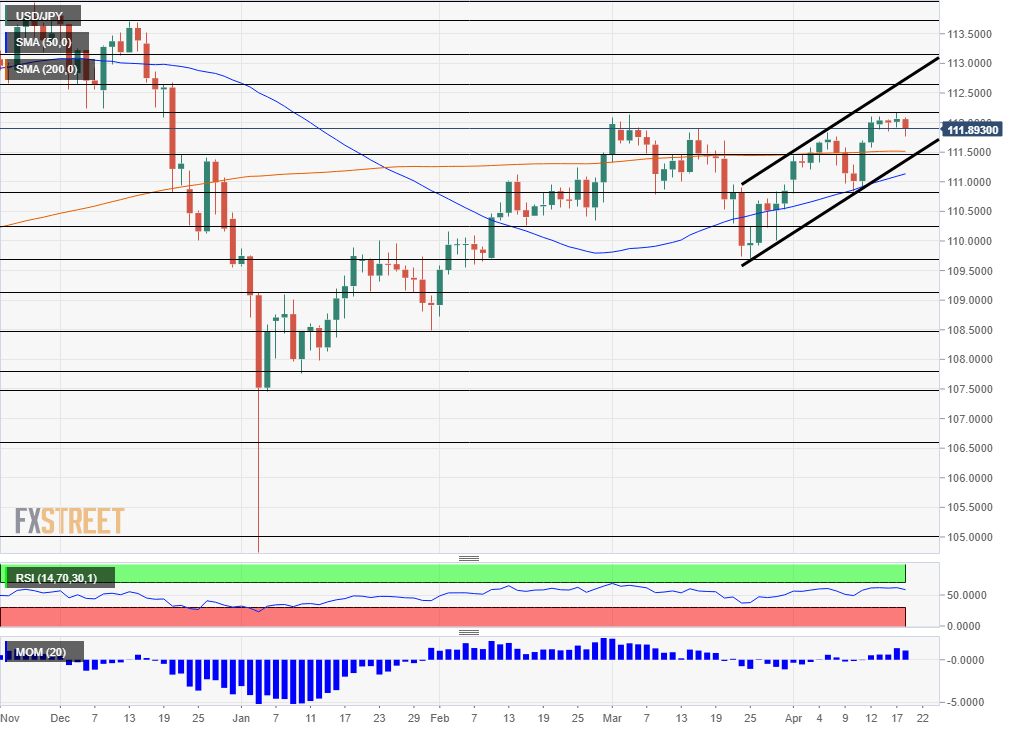

USD/JPY Technical Analysis – Bullish

Dollar/yen continues trading in the uptrend channel (thick black lines on the chart below). The pair also distanced itself from the 200-day Simple Moving Average it captured beforehand and trades above the 50-day SMA as well. Momentum remains positive, and the Relative Strength Index is above 50.

All in all, the bulls are in control.

Critical resistance awaits at the double-top of 112.15 which capped the pair in mid-April and early March. 112.65 capped a recovery attempt in December and also worked as support beforehand. 113.15 was a support line in early December on two occasions. The round number of 114 was a peak in November.

The 200-day SMA meets a peak from early January at 111.50. 110.75 provided support in mid-April and also in mid-March. 110.25 was a support line in February, separating ranges back then. 109.75 was the low point in March and marked the beginning of the uptrend support line.

USD/JPY Sentiment

The consolidation period at the high ground may come to an end if the US GDP disappoints. Concerns about global growth could benefit the yen. Unless US growth remains robust, there is more room to the downside than to the upside.

Get the 5 most predictable currency pairs