The industrial sector remains on a recovery path – that what economists expect ISM’s Manufacturing Purchasing Managers’ Index to reflect in its August report. Nevertheless, that may be insufficient to halt the dollar’s decline.

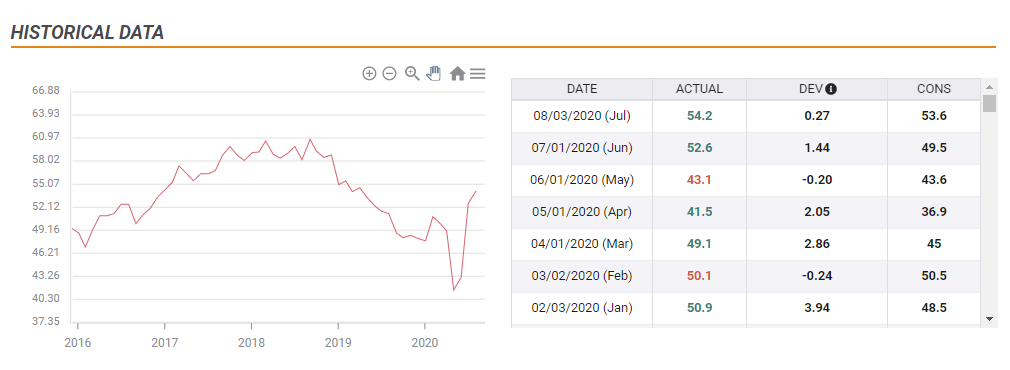

The forward-looking indicator is projected to edge up to 54.5 from 54.2 in July, comfortably above the 50-point threshold that separates expansion from contraction. That would be the third consecutive month of growth after sub-50 scores in March, April, and May, due to coronavirus. However, such a score would also be below a peak of around 60 in 2018.

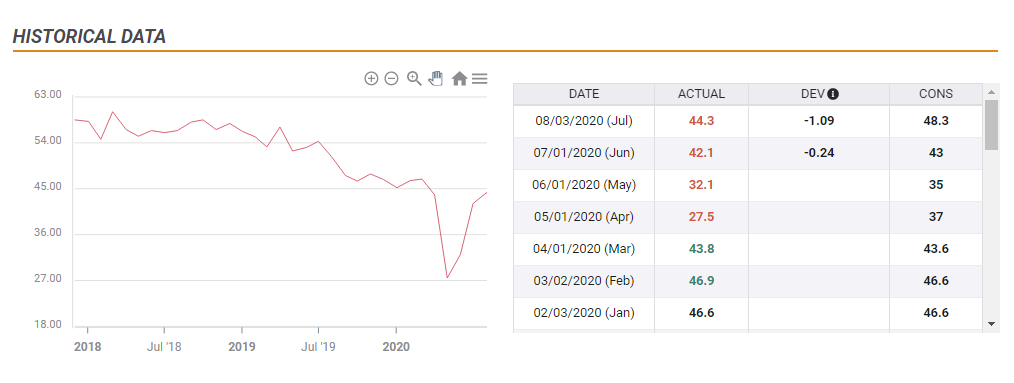

Apart from serving as a snapshot of sentiment for the manufacturing sector, the survey is also eyed as a clue toward Friday’s jobs report. The Employment component of ISM’s publication is still estimated to fall short of expansion territory – scoring 48.3 points.

This gauge of hiring tumbled considerably more than the headline figure, bottoming at 27.5 in April. It made its way up swiftly but has fallen short of estimates in the past four publications.

Bearish dollar bias

If economists have now turned more pessimistic and the employment component surpasses 50, the dollar has room to rise. It would show that industrial employers are bullish and intend to expand their staff – not only restore jobs. Economists will probably revise their forecasts for Non-Farm Payrolls in that case.

Without a positive flip in hiring, the greenback would depend on the headline. A leap from 54.2 to a score closer to 60 would undoubtedly be upbeat and carry the dollar higher – yet that is highly unlikely.

There is a greater chance that the lapse of several government programs at the end of July has hurt the economy and likely hurt sentiment. The pace of the recovery has been slowing down in recent weeks according to jobless claims and other high-frequency data. A miss on the headline would be adverse for the greenback.

What can traders expect if figures are within estimates? In that case, the bias is against the dollar. The world’s reserve currency has been on the back foot since Federal Reserve Chairman Jerome Powell laid out a dovish policy shift. The Fed will prioritize reaching full employment even at the expense of higher inflation – implying lower rates.

While the change in the central bank’s policy has no immediate policy implications, it is having a substantial influence on markets. The prospects of lower rates for several years are weakening the dollar and the bottom is still out of sight.

Conclusion

The ISM Manufacturing PMI is projected to show overall growth but weak hiring in the industrial sector. Only a return to expansion in employment or a considerable surprise in the headline figure would boost the dollar – and such outcomes seem unlikely as the economy slows.

More Markets are Fed-dependent as ever, reaction to elections could surprise – Interview with Lior Cohen

Get the 5 most predictable currency pairs