Under-promising and over-delivering – something that politicians rarely do – is what may happen with expectations for the all-important services sector gauge. The ISM Non-Manufacturing Purchasing Managers’ Index, which is a forward-looking survey for the lion’s share of the US economy, is projected to decline in August.

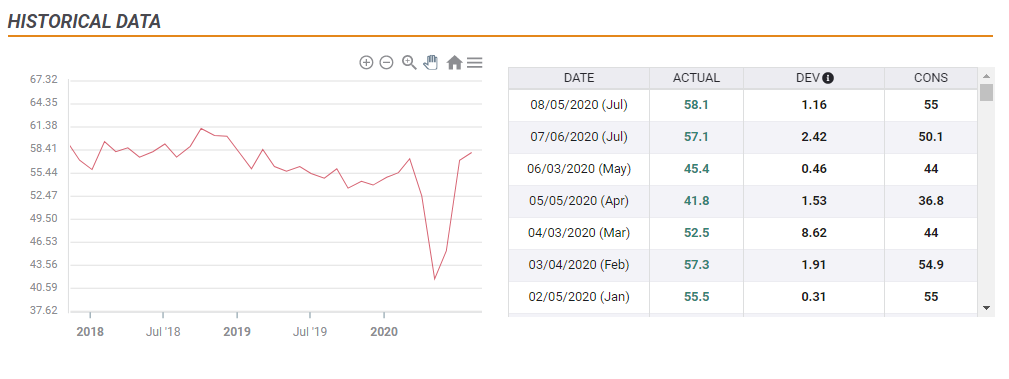

The economic calendar is pointing to a drop from 58.1 points in July to 57 now.

Moreover, economists expect the employment component to plunge from 42.1 to 31.9 points – deep in contraction territory and reflecting a drop in hiring. The figure is critical ahead of Friday’s Non-Farm Payrolls data.

The US economic recovery is slowing down, as seen by several high-frequency indicators such as credit card spending and jobless claims. Several federal emergency programs lapsed at the end of July, leaving a “fiscal cliff” which is causing some pain.

Why expectations are too low

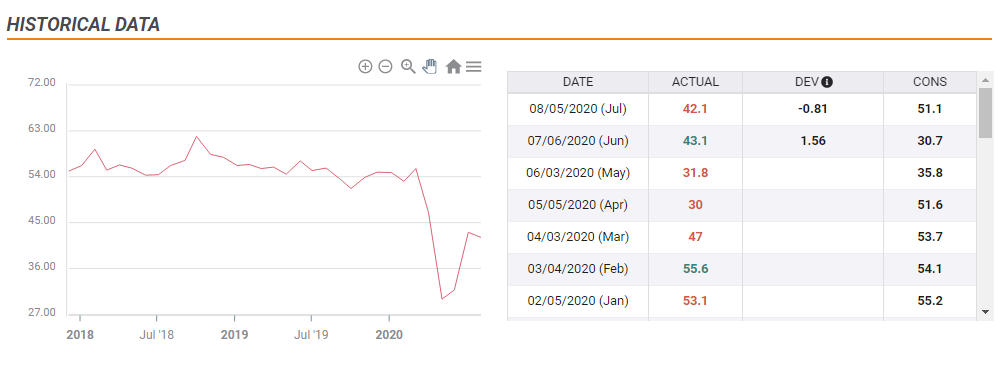

First, the ISM Manufacturing PMI is out, and it beat estimates with 56 compared with 54.5 expected. The correlation between the industrial sector and the services one is strong – it is the same economy. After one data point exceeded estimates and advanced, the second one is less likely to drop.

Looking at the jobs indicator for the manufacturing sector, the picture is more worrying, but not devastating. It progressed to 46.4 – reflecting contraction – but also coming ahead of projections.

It is also essential to remember that while some parts of the economy are struggling, purchasing managers’ are also influenced by the broader mood. Hopes for developing a coronavirus vaccine rose last month and helped push stocks higher – the S&P had its best August since 1986.

Dollar reaction

If the bar is indeed too low, the greenback has room to rise, similar to its response to the manufacturing measure. However, it is also essential to remember that the broader trend is for a weaker greenback.

The Federal Reserve announced a dovish policy shift that continues reverberating through markets, supporting shares and weighing on the dollar. The Fed is prioritizing full employment and would allow inflation to overheat before raising rates. Goldman Sachs, a bank, estimates that borrowing costs will remain depressed until 2025.

While the new thinking has no imminent implications, markets continue benefiting and the dollar remains pressured for the time being.

Therefore, any jump in the world’s reserve currency would potentially provide a selling opportunity.

Conclusion

The ISM Non-Manufacturing PMI and its employment component are projected to decline in August, yet other figures seem more optimistic. However, a potential rise in the dollar will probably be short-lived as the Fed’s dovish shift continues weighing on the greenback.

Get the 5 most predictable currency pairs