A consensus is gathering around a rate cut by the Bank of Canada. Can it send USD/CAD further up? Or is priced in, with a “buy the rumor, sell the fact” move coming? Here are two opposing opinions. Which one has you convinced?

Here is the view from Bank of America Merrill Lynch:

Here is their view, courtesy of eFXnews:

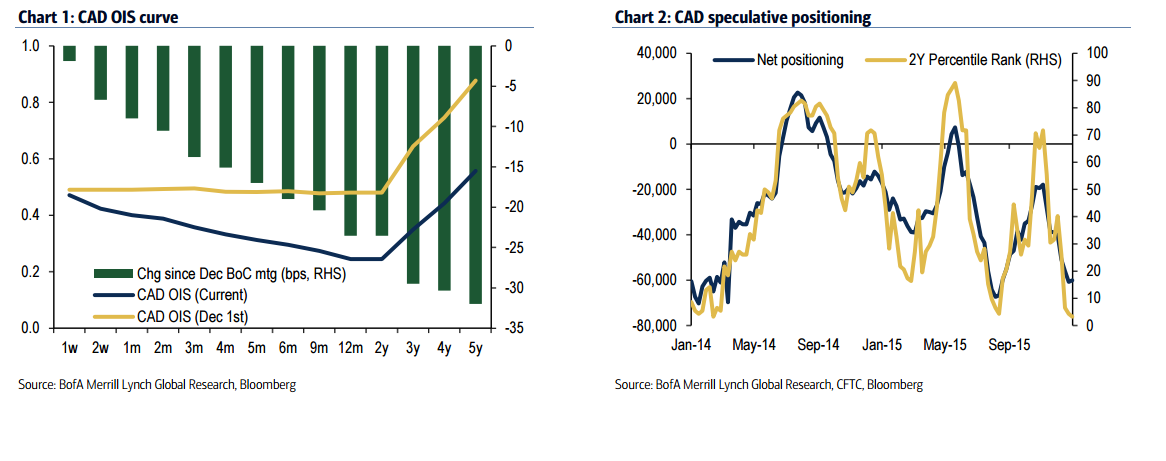

Our out-of-consensus call for a 25bp Bank of Canada cut next week has very quickly become consensus. The market is now pricing a 50% chance of a cut this week (Chart 1), while fully pricing a cut by the March meeting. This is in sharp contrast to the period shortly after the BoC’s December meeting when only 6bps of cuts were priced for the entire year. With less than full cut priced for next week’s meeting, we would expect CAD to remain under pressure in a cut scenario despite its sharp move recently. In the January 2015 surprise cut, USD/CAD rose 2.3%, suggesting that we could still see over a 1% move with a 50% chance already priced in.

Additionally, the tone of the statement will be important. We do not expect a move to forward guidance or other unconventional measures at this week’s meeting (that could come later if the economy continues to struggle). But, a move to 25bps would leave the BoC at a level where forward guidance was implemented in April 2009. A more bearish statement and press conference tone could prompt the market to quickly price the prospect of forward guidance or beyond. The OIS curve remains upward sloping past two years (Chart 1), so the potential market impact is significant. In 2009, the CAD impact of forward guidance was overwhelmed by broader USD trends at that time as the Fed had just embarked on balance sheet expanding QE a month before. This time around, guidance that rates would be kept at current levels for a certain period of time would only reinforce the policy divergence theme between the US and Canada and weaken the C$ further. Moreover, a surprise move to other unconventional measures (QE, negative rates, etc) would drive much more significant C$ weakness with little priced.

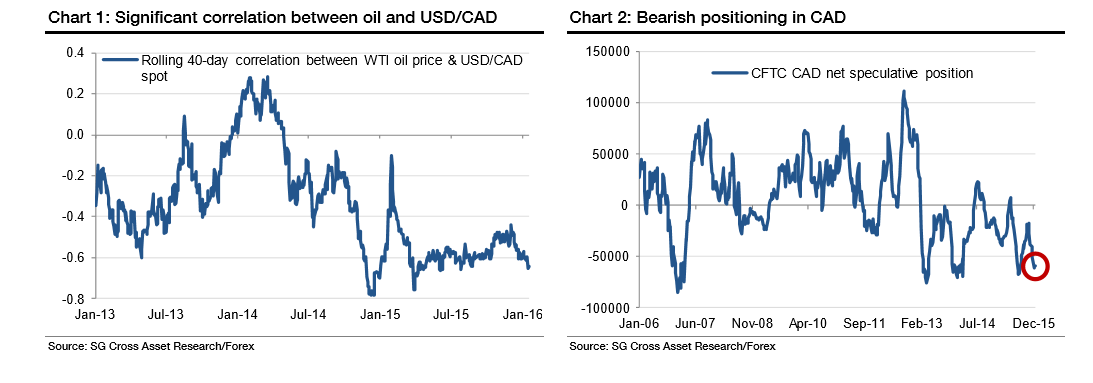

However, even in a no-cut scenario, where stretched short CAD positioning could amplify moves (Chart 2), we would recommend buying USD/CAD on dips. With the risk remaining that oil prices will remain at current levels or move lower, the Canadian economy will continue to struggle amidst larger structural issues in the manufacturing sector. The weakness in the non-energy side of the economy will make it challenging for the BoC to meet its 2016 forecasts with Q4 GDP growth tracking -0.4% (versus their 1.5% forecast).

All told risks remain on the upside for USD/CAD, in our view. The potential for a greaterthan-expected fiscal stimulus is one potential headwind for the pair. Increased discussion of the currency by high level politicians (including PM Trudeau and FinMin Morneau), suggests the political costs of a weaker currency are growing. Greater fiscal stimulus could be one avenue to slow the pace of C$ weakness without sacrificing monetary independence. We still believe USD/CAD would be biased higher in this scenario but to a lesser degree.

And here is the view from SocGen:

A BoC rate cut this week would provide an opportunity to go short USD/CAD at good levels near or at 1.46, for a trade back to 1.40, advises SocGen.

“A more relative value trade on CAD would be to sell NZD/CAD near or at 0.95. Short NZD/CAD is also a medium-term trade that we have recommended for this year,” SocGen adds.

For lots more FX trades from major banks, sign up to eFXplus

By signing up to eFXplus via the link above, you are directly supporting Forex Crunch.